- StableScope

- Posts

- SS #87 - Stablecoin Yield Deal Pleases No One

SS #87 - Stablecoin Yield Deal Pleases No One

Why Mastercard Paid double for Stablecoin Infra | August USDC V2’s 32.67% APY

Karon Pangestu & Marco Manoppo

March 31, 2026

📢 Sponsor | 💡 Telegram | 📰 Past Editions

Good morning.

A bipartisan agreement on stablecoin yield is making its way through Capitol Hill backchannels, with both crypto and banking industry representatives getting private briefings this week on language that could define who gets to offer yield-bearing stablecoins and under what conditions, and neither side likes what they see.

Enjoy the read!

Let us know what sort of coverage you would like to see from the new publication.

If you know anybody who would benefit from this content, please help us spread the word!

In Today's Edition:

Headline: Stablecoin Yield Deal Pleases No One

Quick Bites: Why Mastercard Paid double for Stablecoin Infra

Yield of the Week: August USDC V2’s 32.67% APY

You read and share. We listen and improve. Send us feedback at [email protected].

For daily market updates and airdrop alphas, check out our telegram!

HEADLINE

Stablecoin Yield Deal Pleases No One

State of play: Senators Alsobrooks and Tillis' agreement-in-principle on stablecoin yield is circulating among crypto and banking industry reps, and neither side is happy with what they're seeing.

Crypto industry reps met with legislative staffers on Monday, banking reps on Tuesday, both reviewing language that hasn't yet been released publicly.

Concerns center on whether the proposal would require regulators to draft new rules on permissible activity and how it might restrict stablecoin yield balances.

Major revisions are unlikely, though minor technical tweaks are expected, with industry groups reportedly preparing a counterproposal.

What’s Next: The language is expected to be released publicly this week, with a potential market structure bill markup scheduled for the second half of April.

Why it Matters: Stablecoin yield is a core battleground between crypto-native issuers and traditional banks, and how this language lands will shape who can offer yield-bearing stablecoins and under what regulatory framework.

Our Take: The counterproposal from industry is the move to watch, but with markup weeks away and recess starting now, there's very little runway to meaningfully reshape this language before it gets locked in.

QUICK BITES

South Korea's KB Card taps Avalanche for 'hybrid' stablecoin credit card

Stablecoin Payments go invisible in SEA as Crypto Card business surges.

Why Mastercard paid double for stablecoin infrastructure it could have built.

YIELD OF THE WEEK

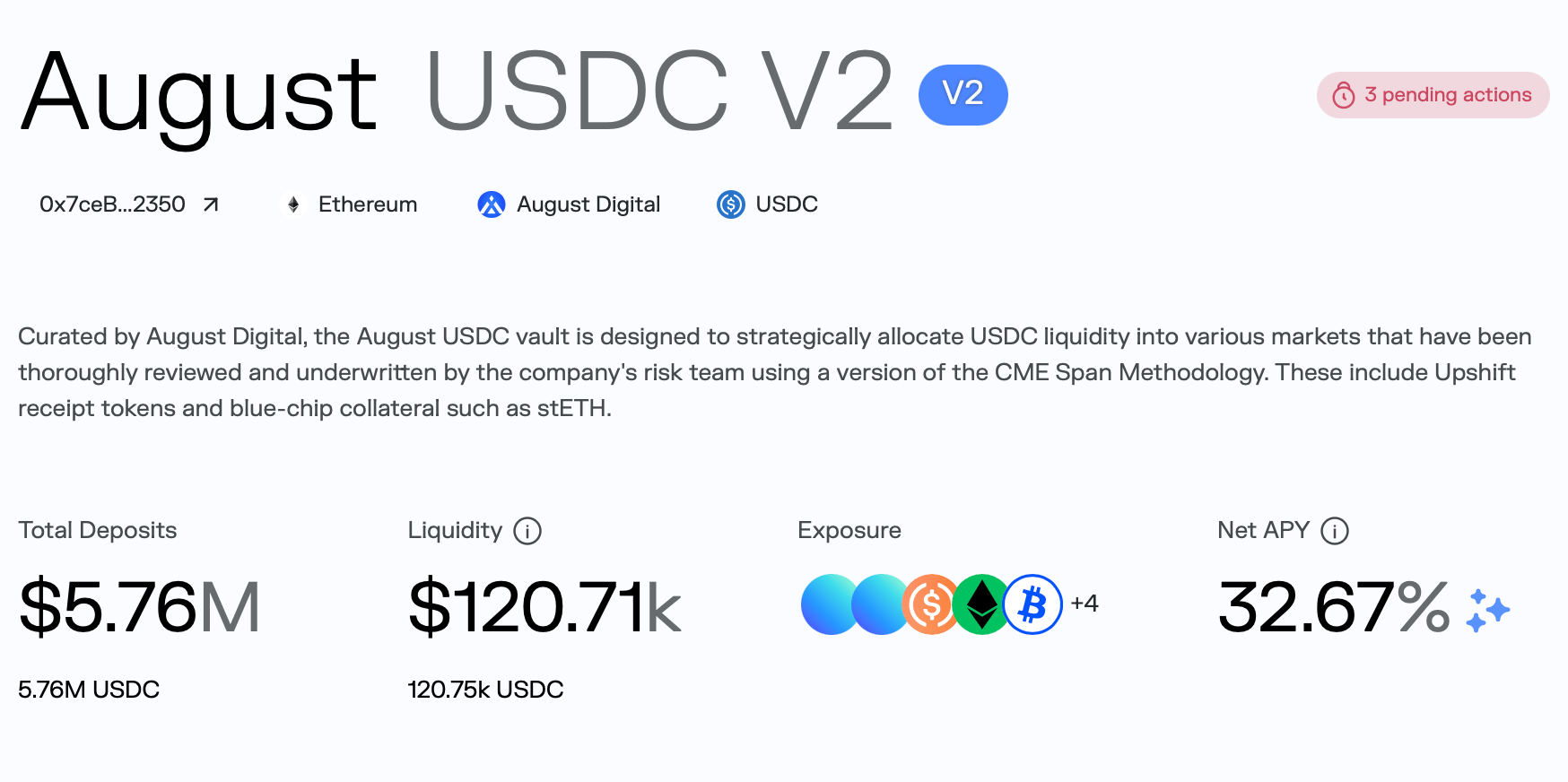

August USDC V2: 32.67% APY

The vault accepts USDC deposits and allocates liquidity across CME Span Methodology-reviewed markets, including Upshift receipt tokens and blue-chip collateral like stETH, with ~$5.76M in total deposits.

Capital is primarily deployed into the August USDC V1 vault with 100% relative cap allocation, maintaining ~$120.71k in available liquidity at a position unit price of 1.016402 USDC.

Yield is generated from lending and liquidity activity across curated Morpho markets, with a base vault APY of 32.43% boosted by 0.24% in MORPHO incentives, net of a 0.24% management fee and 0% performance fee.

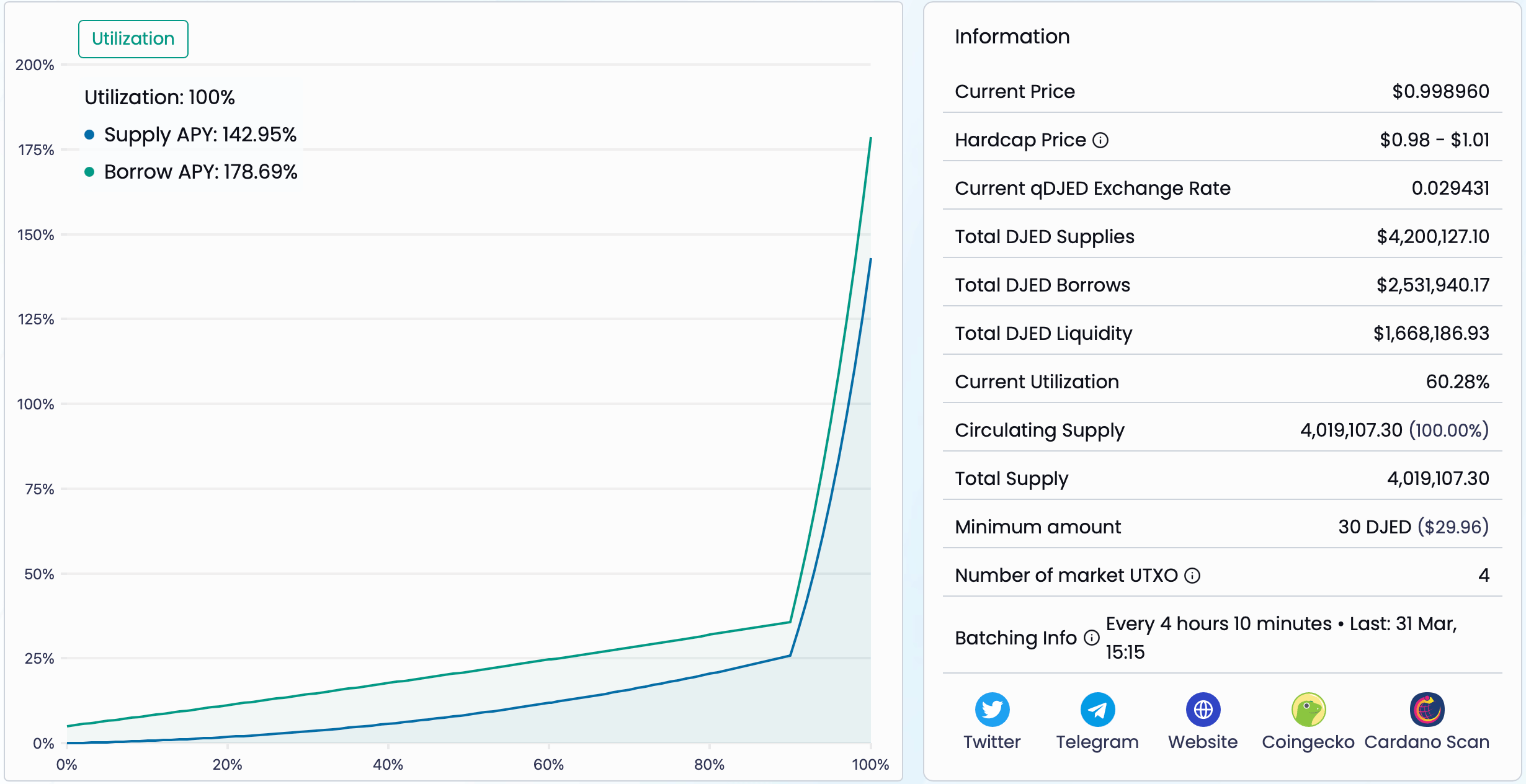

DJED Lending Market (Liqwid): 11.90% APY

The market accepts DJED deposits and lends them out against a wide range of Cardano-native collateral assets, with ~$4.2M in total deposits and ~$1.67M in available liquidity at 60.28% utilization.

Capital is deployed into overcollateralized lending positions across 13 accepted collateral types including ADA, USDA, USDM, and USDCx, with liquidation thresholds ranging from 40% to 81% depending on collateral quality.

Yield is generated from borrowing demand at a 24.69% borrow APY, with 80% of interest income distributed to suppliers and the remaining 20% directed to the protocol treasury, producing an 11.90% supply APY.

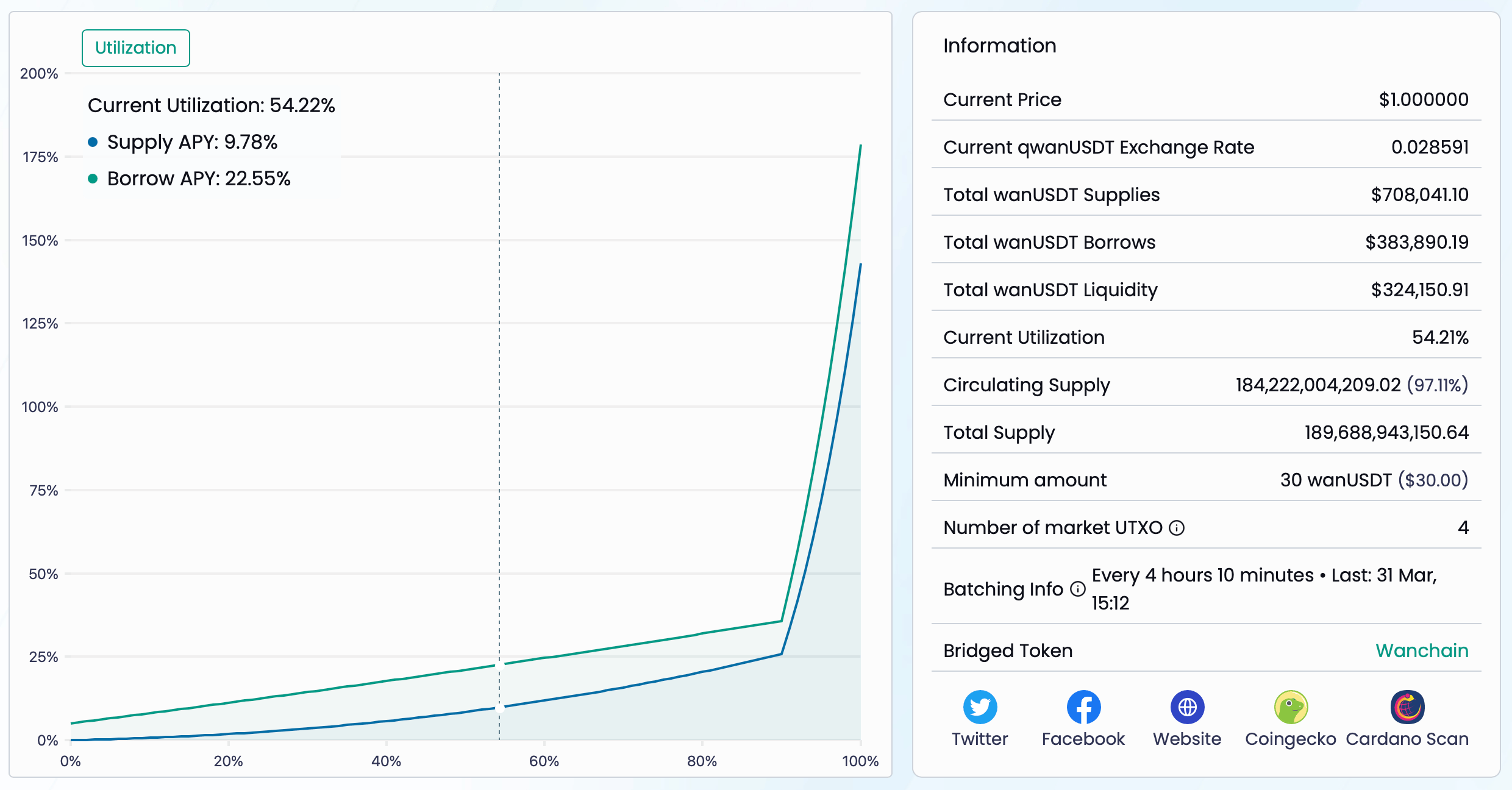

wanUSDT Lending Market (Liqwid): 9.78% APY

The market accepts wanUSDT deposits, a Wanchain-bridged USDT on Cardano, and lends them out against a broad range of collateral assets, with ~$708k in total deposits and ~$324.15k in available liquidity.

Capital is deployed into overcollateralized lending positions across 20 accepted collateral types including ADA, DJED, wanETH, and wanBTC, with liquidation thresholds ranging from 40% to 81% depending on collateral quality.

Yield is generated from borrowing demand at a 22.55% borrow APY, with 80% of interest income distributed to suppliers and the remaining 20% directed to the protocol treasury, producing a 9.78% supply APY.

If you enjoy reading this issue, please consider subscribing. It takes 1 minute of your time, but it would mean the world to us 🙇

Disclaimer: All the information presented in this publication and its affiliates is strictly for educational purposes only. It should not be construed or taken as financial, legal, investment, or any other form of advice.